Monthly pension payments take a sizeable sum of cash out of your monthly salary. Pausing your pension payments is one option if you want extra money coming in. But, how long should you stop paying into your personal pension for and what’s the damage of doing it? Let’s look into this topic.

We all want the same thing. To have a fulfilled career followed by a happy retirement whereby we have enough financial assets (savings, pension, shares, property etc) to support the lifestyle we desire.

The aim is simple, to be happily retired drawing love hearts in the sand!

- 1 Potential Reasons To Pause A Pension:

- 2 Can You Pause Payments Into All Pension Types?

- 3 How To Calculate The Approximate Cost Of Pausing Your Pension

- 4 Calculate The Financial Benefits Expected From What You Plan To Do With The Extra Cash

- 5 Calculate The Difference Between The Cost Of Pausing And Your Anticipated ROI

- 6 Avoid The Domino Effect Of A Long Pause!

- 7 When You Pause The Pension Will Make A Big Difference

- 8 Make A Clear Plan And Go For It!

Potential Reasons To Pause A Pension:

- To make investments in opportunities such as stocks or property.

- To diversify your retirement plan with a broader collection of assets.

- Because money is tight and you could do with the immediate extra income.

The third point isn’t a good reason to pause your pension and could cost you more than it’s worth. If money is tight then it is better to seek other solutions first.

Can You Pause Payments Into All Pension Types?

Most regular payment contributions into pensions can be paused. This is true for all personal pensions and plans for the self-employed.

Legally in the UK all employers have to allow you to opt-out of company pension schemes. Read more about it on the Gov.uk website. Nowadays you can also opt-out of public sector schemes too such as the NHS Pension Scheme. If you’re unsure contact your employer or private pension provider.

How To Calculate The Approximate Cost Of Pausing Your Pension

The information you need is:

- past statements from your employer or pension provider to find out the average percentage your pension has been growing each year.

- how many months/years you plan to pause your pension for.

- how many years it is until you retire and take your pension.

Run the numbers you’ve gathered through a compound calculator. thecalculatorsite.com is an easy tool to use. Put the percentage your pension has been growing per year in the ‘Interest rate’ box. Put the ‘Initial deposit’ as the amount of money that would have gone into your pension during the time it’s paused for. And in the ‘Years’ and ‘Month’s boxes put how long until you retire. Ignore the ‘Regular contributions’ section.

Example Data

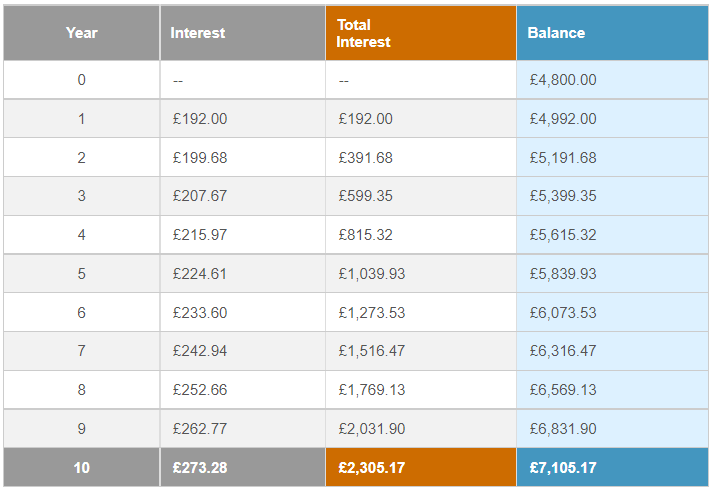

Here’s a simple example. Let’s take someone aged 55, who pays in £400 per month, with an average annual growth rate of 4%, and they plan to retire aged 65 (IE 10 years away). Therefore payments that won’t go into their pension (they’ll receive the cash instead) will be £4,800. Here’s how the numbers come out.

The net result is that this persons final pension will be £7,105 lower once they come retire!

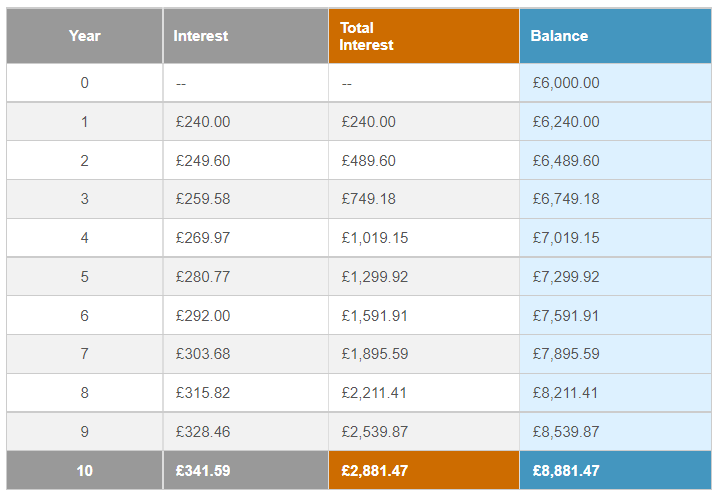

But this doesn’t fully reflect the situation. Because it doesn’t take into account employer contributions. Or if the person in this scenario was self-employed it doesn’t take into account Government contributions. The person would receive £4,800 extra because it hasn’t gone into their pension. But, the actual amount the pension has lost out on would be higher. If the person in this scenario was self-employed they’d have missed out on the Government’s 25% contribution (£1,200). Meaning the real number to calculate is £6,000. Let’s re-run the numbers.

It makes a big difference! £8,881 is the actual amount lower the final pension balance will be! Yet during the 12 months the pension was paused they’d only have received £4,800 extra into their bank.

These numbers are simplified and only designed to give a broad view of the situation. They also don’t take into account tax. But hopefully it demonstrates clearly that pausing a pension can have a significant impact.

Calculate The Financial Benefits Expected From What You Plan To Do With The Extra Cash

If you’re pausing your pension to make an investment you now need to calculate your expected return on your investment (ROI).

Whether it’s the stock market you want to invest in, property, fine wine, or something else – it doesn’t matter. You just want to have a broad understanding of what returns you are expecting to achieve. This can be very difficult, or almost impossible. Especially if it involves buying shares in publicly traded companies.

The best way to go about calculating expected ROI is to work in ranges and averages.

For example, imagine you’re buying shares in a high-growth tech stock to hold for the next decade. You invest the full £4,800 in the stock for it to form part of your final retirement plan. You research the company and formulate a bull case and a bear case. The bull case is that the tech stock’s value triples over the next decade, giving you a £9,600 profit (holding value £14,400). Your bear case shows the stock ending up at the same value after a decade, IE still valued at £4,800. If the performance is somewhere in the middle of those two it will end up at £9,600.

In the scenario above it would have proved a good investment. The final pension balance would be £8,881 lower, but you’d have a stock holding worth £9,600 instead. Meaning it was a profitable decision.

Calculate The Difference Between The Cost Of Pausing And Your Anticipated ROI

Now you have your two numbers of the cost of pausing your personal and your anticipated ROI – go ahead and work out the difference. From there you can see if you think it’s worth it.

Remember to keep the numbers broad and work with ranges of numbers. If you have a high degree of confidence in what you plan to invest in, and it’s showing a high expected ROI, there’s a strong justification for pausing the pension.

Avoid The Domino Effect Of A Long Pause!

The risk of pausing a pension is that you don’t restart the contributions fairly quickly. Because of the compounding effect it can become more and more damaging. The longer you pause it, not only is that less cash going in to give a higher total at the end, but less growth.

It’s a domino effect.

To avoid this from happening be strict with your plans. Aim to get the contributions back up and running as soon as possible.

When You Pause The Pension Will Make A Big Difference

When you pause a pension has a big impact. Someone pausing a pension after 35 years when they’re due to retire in 5 years will have significantly less of an impact than someone pausing a pension after only 5 years. You may have already seen that in the numbers above.

The compound impact will be a lot more brutal if you’re young and have only had your pension setup for a few years.

Make A Clear Plan And Go For It!

If you do pause your pension you want to work hard to get the pension going again as soon as possible. During your project, it could also be wise to re-evaluate the situation and run some calculations if you end up pausing it for longer than initially planned.

Have a clear plan that you’re comfortable with and execute well, there’s not much more you can do then that.

Last update: June 29, 2023