Abundance Investment is a company that lets you put money into sustainable projects in return for capital gains. Projects include wind farms and solar panel installation. It provides an opportunity to make a bit of money over the long-term whilst at the same time contributing to something positive for our lovely planet.

You can invest for as little as £5. The company was launched in 2012, I first invested a small amount of money in a project in 2013. I have now sold my investments to two other people. In this article I’ll go through my experience and who I think this money-making opportunity is good for and who it’s not for.

How does Abundance work and how much money can you make?

Before I get into my experience, I’ll quickly run through how it works and how much money can be made.

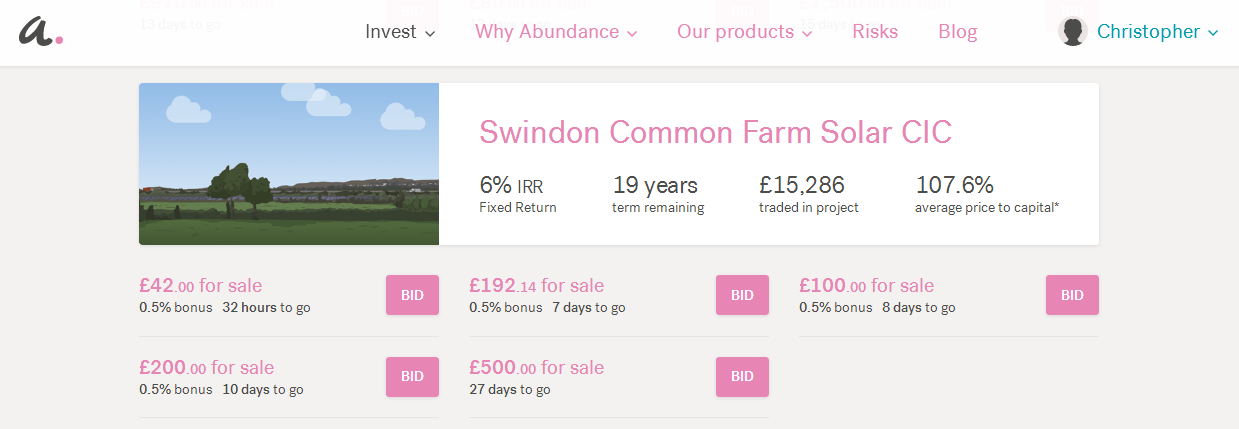

The website is abundanceinvestment.com and it’s free to join as you would expect. Once you are a member you can browse current projects and decide whether to invest or not. Each project goes through a round of funding which gives you a bit of time to invest.

There aren’t always open projects to invest in, at the time of writing none are available. If that’s the case you can either wait or buy other peoples investments off them using the marketplace, that’s how I sold my investments, more on that later in the article.

This type of investment is called a debenture, you may have heard of it before, I’m no expert so if you want to read a proper explanation then Investopedia is your friend.

Once you’ve bought yourself a debenture you should then get a regular return from it. The length of time varies between projects. Many of them last many years. There’s a useful calculator on new projects that allows you to see returns. A quick browse of the marketplace is showing the average project is returning 7% per year, a lot better than a savings account!

What was my time with Abundance like?

It was excellent. I’ll go through everything from start to finish.

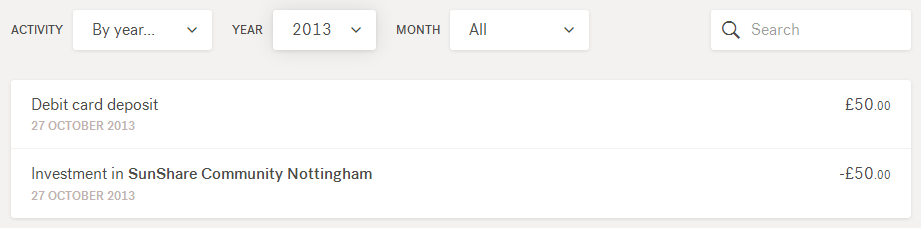

I first invested £50 in 2013 not long after they’d launch. I wouldn’t have been able to remember exact details, but thankfully it’s quite easy to see statements on the website of all past activity. Here is a screenshot of when I invested.

I wanted to invest partly because I liked the idea of contributing to eco-friendly projects, but also to see if this might be something I want to put more money into in the future.

The process of buying the debenture all went smoothly. For this project I would receive 2 payments per year for 20 years, one each June and one each December. In 2014 and 2015 all payments were received on time with no problems. The money builds up in your Abundance Investment account, you can then withdraw it or invest it in other projects. At the end of 2015, I decided to invest the little bit that had built up.

In 2016 the regular payments in the first half of the year were received again with no problem. I had yet to withdraw any money so decided to try it. In the process finding out that there doesn’t seem to be a minimum withdrawal amount which is great. I had a whopping £1.95 in payments in my account in August 2016 so I withdrew them and it was no problem.

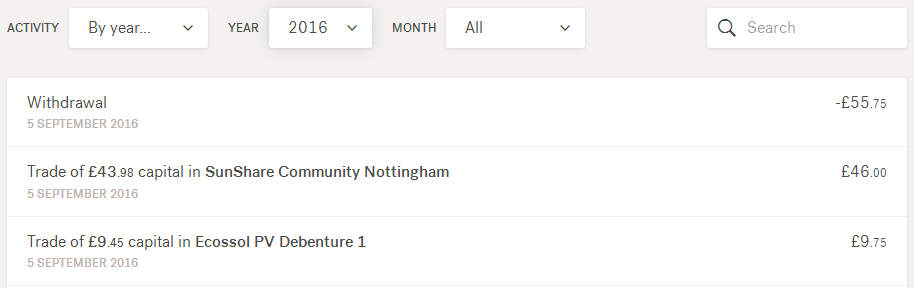

By the end of 2016, I decided I didn’t want to keep the debentures anymore. I had decided to begin focusing on my finances (part of which was starting this blog!), and this would mean selling a few assets for cash.

The process of selling the debentures on the marketplace went very smoothly. They sold quickly and I had no problems.

I withdrew the proceeds of the sales. This means in total I had deposited £50, and in withdrew £57.70 in the two withdrawals I made. I appreciate the raw numbers in Pound Sterling are tiny, but it means a 15.4% return over the 3 years which is certainly better in comparison to having the money in a savings account.

I never had any problems over the years of owning the debentures.

Would I recommend them? Is it safe?

As with all investments, there is a risk with it. If problems occur on a project you may not get back what you expected. The rates of return are estimated, not guaranteed – pretty much the same as any other investment really. It’s obviously riskier than sticking your money in savings accounts, but that is why you are estimated higher returns. During my time using Abundance, it was flawless and I always had complete trust in them and that they were doing a professional job, this was further confirmed when I sold my debentures.

They are regulated by the Financial Conduct Authority and so far there have been no controversies surrounding them which bodes very well.

As for recommending them? It all depends on your circumstances – I would recommend them to certain people, not to others.

For me, I can’t even afford a mortgage! Having long-term investments like this bringing in regular trickles of cash doesn’t make sense. If you are in a similar position then for you, I would say no, it’s not worth it.

But if you are financially secure and looking for a mixed portfolio of investments, then this could make up a nice slice of your pie. You are highly likely to get much higher returns than a savings account, with a lot less risk than the stock market. They sort of sit in between. Debentures like these could also act as a nice part of your pension if you are coming towards retirement age.

All-in-all, as with any investment opportunity, you need to analyze your personal financial situation and you will be able to work out if they are suitable for you. If so then my experience with Abundance Investment was very good and I think you could feel confident in using them.

March 15, 2017